The Rotation Proved It.

Monday opened at 7,595 on the S&P — record territory. NVIDIA cleared 217. Mike validated the Elliott Wave 4 buy live in session and built the calendar before Mic Drop Monday ended. Joe launched his Macross scanner’s first live trade on ENVX. The week started with two Option Strikes posted the same day. SPX touched an all-time high of 7,620 before the session closed.

By Tuesday, the picture shifted. Joe flagged the strangeness: the VIX was ticking higher even as indices made new highs — a divergence that kept institutional conviction in question. Mike noted NVIDIA had dropped below its trend line and needed attention. The geopolitical noise was real: US-Iran talks had broken down, oil opened the week at $88.50 and hit a high of $92 mid-week on Hormuz tensions, and the Strait remained a live risk.

Friday delivered the gut-punch. Nonfarm payrolls printed 172,000 — more than double the 80,000 consensus. Joe called it immediately: “When the jobs number runs that hot, the Fed’s hand gets forced — and that’s not good for semiconductors or tech. That’s your signal to rotate.” VIX spiked from 16 to 21.51 — its highest print in over a month. The Nasdaq dropped 4.7% on the week, its worst since April 2025. The rotation that had been building all week — out of XLK, into insurance, healthcare, and financials — accelerated into something you could see in real time.

The week ends with a different market than it started. Two Option Strikes active. A sector rotation live. And the same question the community has been building toward all week: did you check IV before you picked the structure?

S&P 500 · 1-Year Daily · Red: 50-day SMA · Blue: 200-day SMA · Powered by TradingView

- Nonfarm Payrolls 172k vs 80k — massive beat raised Fed rate hike probability ~85% by year-end. Sold semis, bought insurance.

- Broadcom earnings — beat EPS, +143% AI revenue YoY, missed revenue. Semis down 4-7% at Thursday open.

- Strait of Hormuz effectively closed — WTI opened the week at $88.50, closed at $90.54 on Iran geopolitical tension. Inflationary pressure elevated.

- NVDA Elliott Wave 4 breakout above 217 — Mike's line in the sand. Triggered both the Option Strike and the Triple Threat framework.

- RSP new highs — equal-weight S&P confirming broad market participation beyond mega-caps through mid-week.

- Insurance sector rotation (HUM, PGR, CB, TRV) — rate hike environment lifts float returns. Ken's AI spreadsheet pointed the way.

- Healthcare names (LLY, AMGN) — defensive rotation continuing out of XLK.

- NVDA & ENVX — both Option Strikes active. NVDA stop: close below 217. ENVX max risk capped at premium paid.

- HD breakout above 324 (50-day MA) — Wave 5 buy trigger. Calendar at 350 target on confirmed close.

- CRWD split June 25 — 4-for-1. Any active positions should be closed before split date.

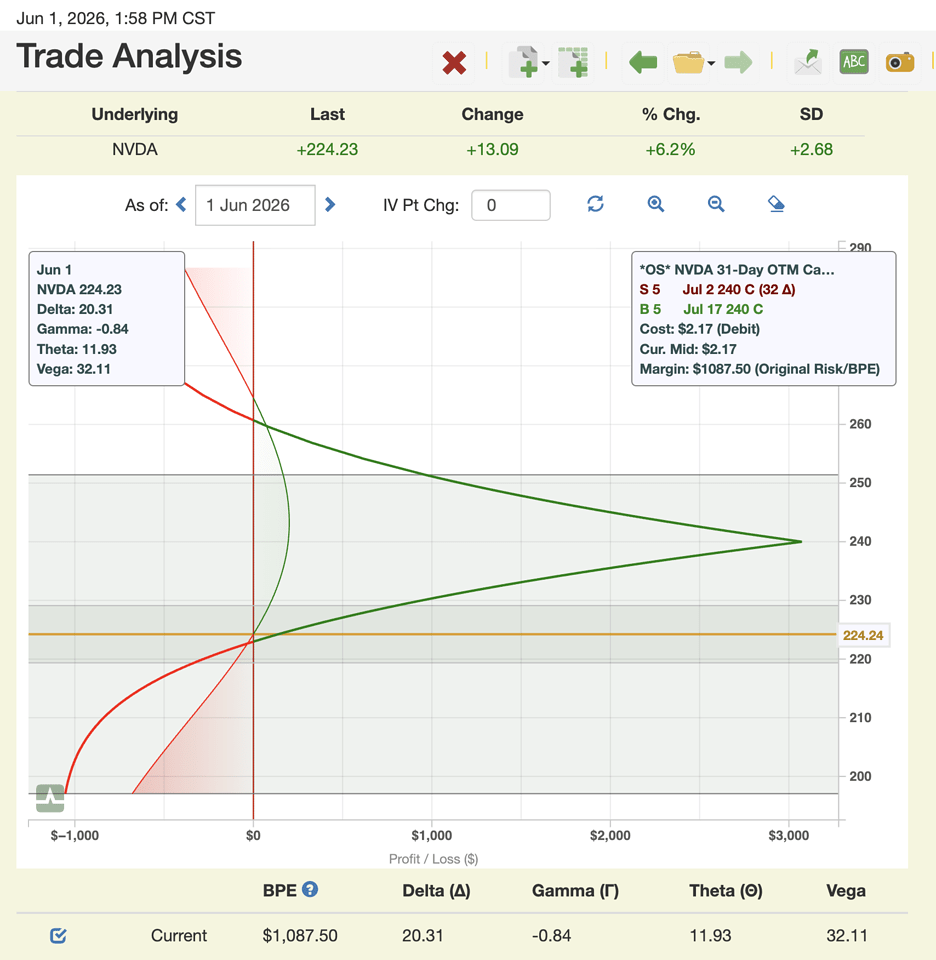

NVDA cleared 217 Monday morning. Mike validated the Elliott Wave 4 buy live in session, confirmed IV was rising alongside price, and built the OTM call calendar before Mic Drop Monday ended — short near Jul 2, long Jul 17. Direction, theta, and vega all aligned with the bullish thesis at once. Mike's words after building it: "So there, ladies and gentlemen, is a soup to nuts triple threat trade matching up prognosis with Greeks and a very, very good trade indeed." A milestone too: the club's first-ever Elliott Wave Option Strike.

The market had other plans. NVDA reversed hard with the Friday selloff, dropping below the 217 line in the sand that Mike had defined before entry. The position was closed at approximately 50% of the premium paid — a loss of roughly $500 on the ~$1,000 at risk.

This is what risk-first looks like in practice. The stop was defined before the trade was placed. When it triggered, the decision had already been made. The setup logic was sound — the market moved against it. A well-managed loss on a well-constructed trade is not a failure. It's the system working exactly as designed. Check the forum post for Mike's full update.

Joe's Macross scanner has been a talked-about system for weeks. Monday was the first live trade. ENVX flagged on the scanner — 7 prior signals on this system with a median move around 35%. IV was flat-to-up. Joe entered the 11-strike 30-delta call at July expiry, filled around $0.52, roughly $520 at risk.

Half size. Deliberate. When launching a new system live, going half-size on the first real trade lets you get honest fills and validate execution without overexposing capital. No stop loss needed — the structure itself limits risk to the premium paid. Joe made it plain: "This system doesn't use stop losses — it works great by limiting your risk to what you pay for the thing. Then call it good, let it run."

PVH gapped down hard on earnings. Mike entered a bear-call spread at the 90/100 strikes, collecting $1 credit against $900 max risk. The setup works because 90 had served as resistance before the earnings gap — that prior ceiling gives the short strike extra structural support.

Mike called it the "bigger tree": when prior resistance sits exactly at your short strike, you have two layers of ceiling working for you — the spread mechanics and the technical level. GTC buyback order placed. Clean execution, defined risk, no ambiguity about exit.

TWLO had just broken out above $200 on massive institutional volume. Bullish prognosis, clean technical confirmation. And then Mike stopped. IV was falling. That single variable changed the structure.

A debit call spread with falling IV means fighting IV crush on top of needing directional accuracy. A bull-put credit spread turns falling IV into an ally. Mike placed the 190/195 put credit spread for ~$0.60, 14 days to expiry. The lesson was the point: "I am hell-bent on having everybody here look at IV before they put on a trade. It's so critical. Everybody, it's so, so, so critical."

Tony's Morgan Stanley BWB has decayed to nearly risk-free. Time and price worked together. The position is now holding with minimal downside exposure and Mad Hatter conversion options on the table.

This is what "detach and react" produces over time. The original max risk was defined before entry. Tony managed by the rules, not by P&L anxiety. The position didn't become risk-free because Tony got lucky — it became risk-free because the structure was sound and the prognosis held. The two things compound.

Option Strikes are the official weekly trade ideas posted to the forum and WhatsApp for members to replicate. Two were posted on the same day this week — an unusual double-signal session that doesn't happen often.

NVDA broke above the 217 pivot, validating the Elliott Wave 4 buy. IV was rising alongside price. Mike built the OTM call calendar — short near Jul 2, long Jul 17 — aligning delta, theta, AND vega with the bullish thesis. That is the Triple Threat definition executed precisely.

Line in the sand: close below 217. Conservative Elliott Wave target: $250 by end of July.

View forum post →

Joe's Macross scanner flagged ENVX — 7 prior signals on the system, median moves ~35%, IV flat-to-up. First live trade on this system, so Joe went half size to validate execution without overexposing capital.

11-strike 30-delta call, July expiry. Filled ~$0.52. No stop loss needed — max risk is capped at what you paid. Let it run.

View forum post →IV direction was the deciding variable in every live trade entered this week. Not direction. Not price levels. IV.

On NVDA Monday, IV was rising alongside price — a broken-wing butterfly (negative vega) would have fought that. The calendar aligned all three Greeks with the bullish thesis instead. Triple Threat.

On TWLO Thursday, the directional prognosis was bullish and the technical breakout was clean. But IV was falling. Buying calls into falling IV means fighting IV crush on top of needing directional accuracy. Mike sold a bull-put credit spread instead — turning the falling volatility into an edge rather than a headwind.

IV direction tells you whether to buy or sell premium. Directional prognosis tells you which side to be on. You need both before a strategy makes structural sense. Every trade built this week followed that framework. The week made the lesson impossible to miss.

172,000 jobs. Nobody expected it. Markets that started the week at all-time highs ended it with the Nasdaq's worst week since April 2025. Semiconductor stocks wiped a trillion dollars in value on Friday alone. The rotation that had been building quietly all week — out of tech, into insurance, healthcare, and financials — accelerated into something you could see in real time.

Between Monday's open and Friday's close, every trade that worked this week shared one thing: the strategy was chosen after the IV prognosis was formed, not before. TWLO's credit spread worked because IV was falling — and the structure used that. The PVH snipe worked because prior resistance sat exactly at the short strike — two layers of ceiling. Tony's Morgan Stanley BWB required nothing from the market this week because the structure was designed to need nothing.

That's the framework. The jobs number was the test. The discipline is what passed.

Your trades belong in the room.

Bring a setup you're working through. Bring an adjustment question. Bring a position that's confusing you. Coach-guided review is how this community gets better together. All recordings, resources, and session links are in your dashboard.

Go to the Trade Club Dashboard